Table of Content

As intended, the main beneficiaries were homeowners at the lower end of the middle class with incomes in the $50 to $150 monthly range, persons who in the private market would have lost their homes. The Home Owners’ Loan Corporation was a federal program established in 1933 to provide relief to troubled mortgage borrowers and their lenders. The Home Owners’ Loan Corporation operated by purchasing mortgages from private lenders and issuing new mortgages to the borrowers.

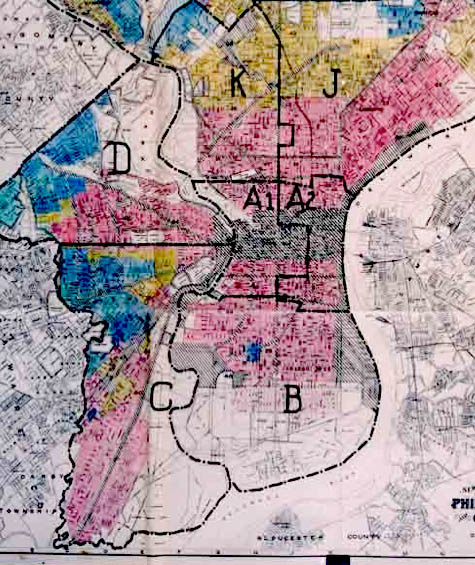

These maps document how loan officers, appraisers and real estate professionals evaluated mortgage lending risk during the era immediately before the surge of suburbanization in the 1950’s. Neighborhoods considered high risk or “Hazardous” were often “redlined” by lending institutions, denying them access to capital investment which could improve the housing and economic opportunity of residents. Between 1933 and 1935, the HOLC made slightly more than one million loans. At that point it stopped making new loans and then focused on the repayments of the loans. The typical borrower whose loan was refinanced by the HOLC was more than 2 years behind on payments of the loan and more than 2 years behind on making tax payments on the property. The HOLC eventually foreclosed on 20 percent of the loans that it refinanced.

Operations Of Home Owners’ Loan Corporation

In 1939, the company lowered rates to 4 1/2 per cent for a wide range of the borrowers. The HOLC loans typically amortized which meant that they would have equal monthly payments each month for the loan. It offered money at 5 percent, provided insurance for its loans through the Federal Housing Authority and the Federal Savings and Loan Insurance Corporation, and allowed up to twenty-five years for repayment. Every loan situation was handled individually, including personal visits to prevent default.

Perhaps ironically, HOLC had issued refinancing loans to African American homeowners in its initial "rescue" phase before it started making its redlining maps. The racist attitudes and language found in HOLC appraisal sheets and Residential Security Maps created by the HOLC gave federal support to real-estate practices that helped segregate American housing throughout the 20th century. When the HOLC was started some .people expressed the fear that the experiment of direct Government lending to homeowners in default on their mortgages and taxes might cost the Treasury huge losses. They knew that through vigorous public and private action the downward spiral of depression could be reversed, and that these loans would be sound assets which would be repaid in full. HOME OWNERS' LOAN CORPORATION. For middle-class America the Home Owners' Loan Corporation, founded in 1933, was a crucial New Deal benefit. Americans had always held to an ideal of individualism that included a home of one's own; but in the years leading up to the New Deal, only four out of every ten Americans managed to attain that status.

How did the Federal Housing Administration help the Great Depression?

The urban reformer Charles Abrams pointed out that, on average, the HOLC refinanced the mortgages it purchased for only 7 percent less than the previous, admittedly inflated, value of the property in question . The HOLC, for example, might refinance a $10,000 mortgage as if the initial amount loaned to the home owner had been $9,300, but that figure—$9,300—could still be significantly higher than the current deflated market value of the property. Under this arrangement, lenders only had to forego a small part of their capital, plus they received government-backed bonds in place of frozen mortgages. On the other hand, by propping up the face values of its refinanced mortgages, the HOLC compelled home owners to repay inflated 1920s mortgage loans with deflated 1930s wages.

HOLC was established as an emergency agency under Federal Home Loan Bank Board supervision by the Home Owners’ Loan Act of 1933, June 13, 1933. Foreign Exchange Regulation Act to regulate certain payments dealing in foreign exchange, securities, import & export of currency. National Industry Recovery Act It set up the National Recovery Adminstration and set prices, wages, work hours, and production for each industry. The Great Depression and Credit During the Great Depression of the 1930s, thousands of banks folded, robbing millions of Americans of their savings. Savings in banks were never insured, and as more people and businesses tried to withdraw their funds, the banking crisis intensified. As long as all parties knew the seller was becoming a cosigner and was being removed from the deed, and the lender would lend the money under these conditions.

Is there greater inequality in HOLC?

In response, Congress rapidly created the Home Owner's Loan Corporation. The HOLC agency was established in the context of the FDR’s New Deal Programs that encompassed his plans that included Relief, Recovery and Reform to fight the problems and negative effects caused by The Great Depression. HOLC also supported the mortgage industry by refinancing difficult loans and also increasing the institution’s liquidity. The HOLC was unable to make loans in the future and focused instead on repayments of loans. It is important to note that the B&L was a direct reduction loan where certain amounts of principal was due every month.

75th Anniversary of the Wagner-Steagall Housing Act of 1937 The Home Owner’s Loan Corporation was created in 1933 to provide mortgage relief to home owners at risk of losing their homes through foreclosure. The HOLC was established in June 1933 to help distressed families avert foreclosures by replacing mortgages that were in or near default with new ones that homeowners could afford. A 2020 study in the American Sociological Review found that HOLC led to substantial and persistent increases in racial residential segregation. A 2021 study in the American Economic Journal found that areas classified as high-risk on HOLC maps became increasingly segregated by race during the next 30–35 years, and suffered long-run declines in home ownership, house values, and credit scores. Furthermore, it offers institutions, loan associations and other real estate investors to exchange defaulted mortgages for $2 3/4 billion in cash and Government bonds.. Through earnings on its loans, it has paid its own administrative expenses, and offset the real estate losses which it had to meet.

What is the Home Owners Loan Corporation quizlet?

Far from "ironically" issuing a few loans to African-Americans in an "initial phase" and then becoming a major promoter of redlining, HOLC actually refinanced mortgage loans for African-Americans in near proportion to the share of African-American homeowners. The pattern of loans had basically no relationship to the "redlining" maps because the program to create the maps did not even begin until after 90% of HOLC refinancing agreements had already been concluded. As for private lenders, though Kenneth T. Jackson's claim that they relied on the HOLC's maps to implement their own discriminatory practices has been widely repeated, the evidence is weak that private lenders even had access to the maps. By contrast, it is well documented that private lenders understood which neighborhoods the FHA favored and disfavored; suburban greenfield developers often explicitly advertised the FHA-insurability of their properties in ads for prospective buyers.

While the ultimate use of the HOLC residential security maps is a subject of debate, it is clear that the HOLC maps compiled the common understanding of local-level lending decision makers of the risk in the neighborhoods of their cities. Consequently, the HOLC maps document which areas were considered lower risk, and therefore preferred for loans, and higher-risk areas where lending was discouraged. The maps document the neighborhood structure of cities and indicate areas which may have been subject to “redlining” by banks when making lending decisions. According to a paper by economic historian Price V. Fishback and three co-authors, issued in 2021, the blame placed on HOLC is misplaced.

HOLC was officially shut down in 1951, after its last assets were transferred in 1951 to lenders from the private sector. These questions are approached through the spatial analysis of the HOLC map archive, and the degree to which the old grading corresponds with current neighborhood economic and racial/ethnic status. This is then compared with overall city-level indicators of segregation and economic inequality.

Consequently, the term of the loan could not change unless the loanee did not pay the loan. Due to the fact that HOLC obtains loans by providing a bond value equal to the amount of principal owing by the borrower, most of the lenders have benefited from the sale of their loans. This is because of the high-interest rate which if not paid at the right time, accumulates. Home Owner’s Loan Corporation was established to help manage this situation. Before the pandemic devastated minority communities, banks and government officials starved them of capital.

At the same time, they enabled banks, insurance companies, savings and loan associations and other real estate investors to exchange defaulted mortgages for $2 3/4 billion in cash and Government bonds. This new life blood saved many hundreds of financial institutions--permitting them to pay off their depositors or investors as necessary and to remain in business. The Home Owners' Loan Corporation was a government-sponsored corporation created as part of the New Deal. The corporation was established in 1933 by the Home Owners' Loan Corporation Act under the leadership of President Franklin D. Roosevelt. Its purpose was to refinance home mortgages currently in default to prevent foreclosure, as well as to expand home buying opportunities.

The HOLC shut down its operations April 30th of 1951 with “a slight profit,” contrary to the belief that taxpayer money will be lost in this business [88. The Home Owners Loan Act in 1933 turned out to be among the most popular policies to emerge in the initial 100 days in the New Deal. Here You got Some Questions Which people Ask Most of the time on Google. HOLC was only available to homes owned by nonfarm owners, valued not more than $25,000.

The HOLC stopped its lending activities in June, 1936, by the terms of the Home Owners' Loan Act. The historian David Kennedy did not exaggerate in claiming that the HOLC and the housing legislation it set in motion "revolutionized the way Americans lived." Diminished wages, widespread unemployment, and few, if any, refinancing options made it difficult for home owners to meet monthly mortgage payments during the Great Depression.

Long-term racial discrimination caused by the HOLC leaves lasting long-term impacts on a population's health, education, and income. Home Owners’ Loan Corporation , former U.S. government agency established in 1933 to help stabilize real estate that had depreciated during the depression and to refinance the urban mortgage debt. It granted long-term mortgage loans to some 1 million homeowners facing loss of their property. Home Owners' Loan Corporation , former U.S. government agency established in 1933 to help stabilize real estate that had depreciated during the depression and to refinance the urban mortgage debt. The HOLC, which was under the supervision of the Federal Home Loan Bank Board, did not actually lend money to home owners.

No comments:

Post a Comment